Ether (ETH) experienced a steep 9.5% correction on Dec. 11. However, buyers quickly stepped in to defend the $2,220 support. Traders are now beginning to question whether the Ethereum network has what it takes to reinstate the bullish momentum in Ether price.

It is worth noticing that the correction aligned with the broader cryptocurrency market, with Ether’s 6.7% decline in the last 24 hours closely matching Bitcoin’s (BTC) -5.4% and XRP’s (XRP) -6.6% performances.

Are futures markets the sole reason for the ETH price correction?

Naturally, excessive leverage is typically blamed for price movements that partially revert within minutes. The truth is that only $86 million in ETH long future contracts were forcefully terminated in the past 24 hours. This number pales in comparison to the $7.8 billion open interest in ETH futures, indicating that a significant portion of the $600 billion decline in available positions resulted from traders themselves.

Binance’s Ether futures open interest declined by 6.8% in the past 24 hours, according to Coinglass. Similar impacts are evident on Bybit and OXK exchange, with -5.2% and -6.7% changes in ETH futures’ open interest, respectively. In contrast, CME and Deribit saw flat open interest, suggesting that retail traders bore the brunt of the impact.

One could argue that the correction was healthy since retail traders using excessive leverage were flushed out of the market, whether due to their stop losses or the exchanges’ liquidation engines. However, Ether investors now have additional reasons to believe that the $2,400 level seen on Dec. 9 has become a distant dream.

High Ethereum network fees propel competing blockchains

For starters, the Ethereum network’s average transaction fee presently stands at $7.90, a level prohibitively costly for most users and use cases. This fee also burdens opening and closing layer-2 operations, even when batching transactions to reduce costs further. Such measures are essential to maintain the same security level during parallel processing.

Some analysts and investors argue that Ethereum’s high fees signal success rather than failure, as the ecosystem’s layer-2 solutions have grown to a massive $15.9 billion in total value locked (TVL). Arbitrum One and the Optimism mainnet dominate the scene with an 80.9% combined market share, according to L2beat. Application-driven blockchains like dYdX v3 and Immutable X also play their role.

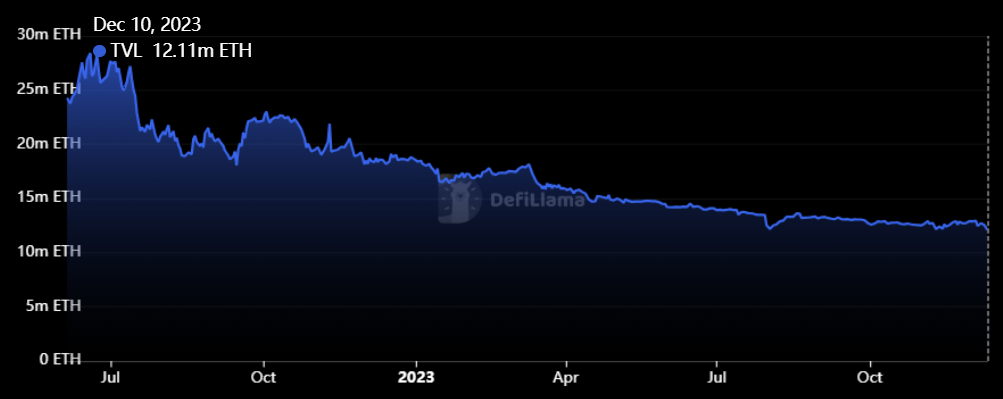

In terms of TVL, the Ethereum network has been losing market share to competitors. For instance, since Nov. 30, BNB Chain’s TVL has declined by 2% in BNB (BNB) terms, while the Solana network experienced a 5% TVL increase measured in SOL (SOL). In comparison, the Ethereum network faced a 7% decline in the same period, reaching its lowest level in over three years at 12.1 million ETH.

The decline in Ethereum’s TVL could have been offset by the growth of its Ethereum Virtual Machine-compatible scaling solutions, including Polygon. Thus, one should examine the market share of the Ethereum network’s decentralized exchanges (DEX) to determine if competing base-layer solutions have also benefited.

Related: Immutable expands Web3 gaming payment options with Transak integration

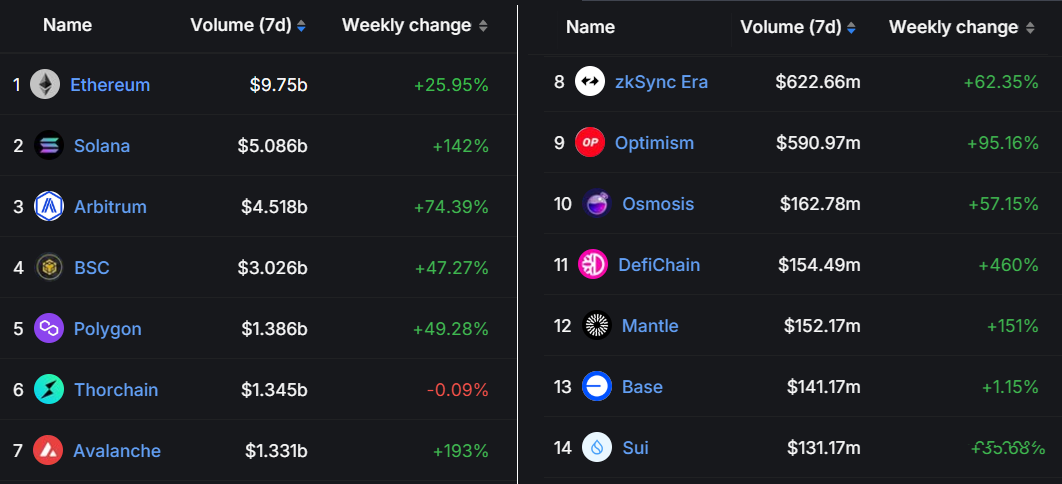

Notice that the Ethereum network remains the undisputed leader despite having significantly higher fees than its direct competitors. However, Ethereum’s weekly 26% gains in DEX volumes are far smaller than Solana’s, BNB Chain’s, or Avalanche’s at 142%, 47% and 193%, respectively. In essence, most of the recent DEX volume gains occurred outside Ethereum’s layer-2 ecosystem.

Now, this data does not necessarily imply that Ether’s $2,400 high on Dec. 9 was driven by exaggerated derivatives leverage — quite the opposite. Additionally, given that the Ethereum network’s TVL decline seems to be compensated by growing demand from its scaling solutions, there is no reason to believe that the Dec. 12 price crash is a telling sign of further price correction.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.